Behind the U.S. stock chain: the narrative is very lively, the market is very cold, can old bottles of new wine become the second curve engine of the bull market?

Author: Frank, PANews The

listing of US stocks has become a hot topic in the recently deserted market.

On March 8, Swiss tokenization issuer Backed launched the Coinbase stock token wbCOIN on the Base chain, allowing users to trade with USDC through CoWSwap, claiming that it is 1:1 pegged to the value of $COIN shares and has legal claims. Although Backed emphasizes that it has no official affiliation with Coinbase, this move has sparked heated discussions in the community: Will the tokenization of US stocks usher in a new growth cycle? In the continuous downturn of the market, can the "new bottle of old wine" of stock tokenization become a new narrative to build the bottom?

The narrative takes the lead, and the value comes later: the hot and cold contrast of US stock tokenization

With the coming to power of the pro-crypto Trump administration, the litigation relationship between the US SEC and Coinbase has also ended. In early 2025, Jesse Pollak, head of the Base protocol, said on X that Coinbase is considering bringing tokenized $COIN shares to the Base network for US users. But it will take time for Coinbase to launch this business compliantly.

Backed's quick action was one step ahead. According to official information, Backed was founded in 2021 and initially received investment support from institutions such as Gnosis and Semantic, and Backed's headquarters and operations are mainly for the global market, and its products are issued under the EU regulatory framework, comply with MiFID II compliance requirements, and have passed the EU's prospectus.

However, wbCOIN is not Backed's first stock tokenization product, as as early as July 2024, Backed launched NVIDIA's tokenized stock trading in conjunction with INX. In addition, Backed has also launched tokenized products with various stock assets such as S&P 500 and Tesla. It's just that when these products were launched, the focus of the market was not on the topic of securities tokenization, and today's market urgently needs some reasonable narratives to rebuild confidence.

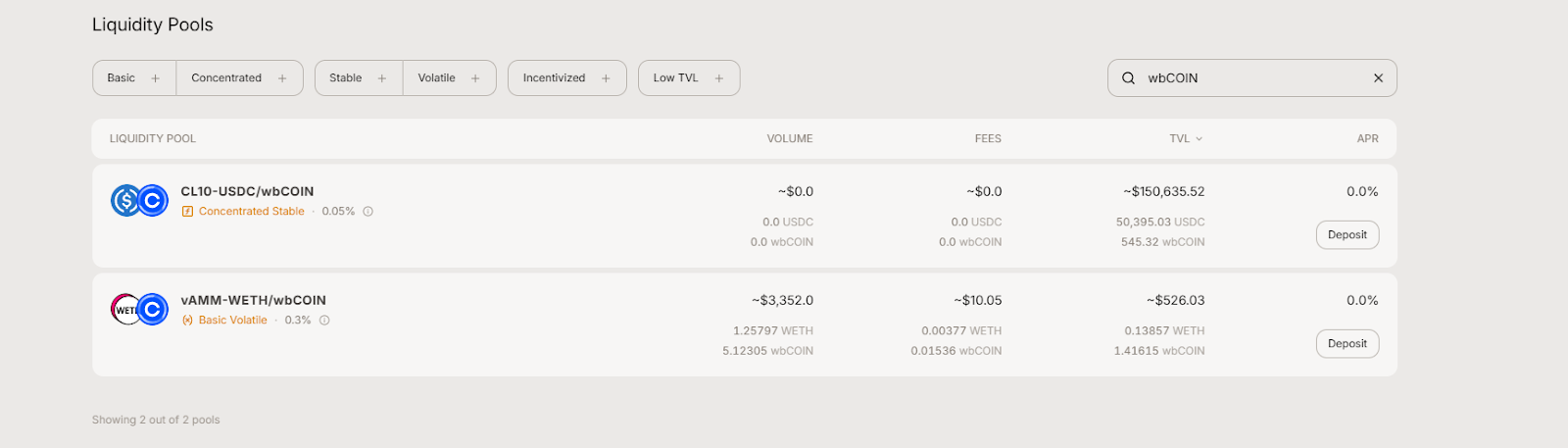

However, it is not just because Backed's products are not suitable for the US market or the market is sluggish. The trading popularity of wbCOIN after its launch is obviously not as hot as the topic. As of March 11, wbCOIN had a TVL of approximately $4.42 million.

According to Aerodrome's data, its trading volume is only $3,352. It's not even as popular as a newly issued MEME coin.

– >

– >

this downturn isn't just due to wbCOIN's short launch time – BNVDA, another product that went on sale earlier, also had a trading volume of just $113, which was also unnoticed.

Despite the hot concept, the current US stock tokenization market is still in its early stages, and its scale and activity are very limited. Perhaps, tokenized products from Coinbase may trigger more trading enthusiasm.

Tokenized U.S. stocks: Old bottles of new wine, compliance is the primary threshold

In fact, moving U.S. stocks to the blockchain is not a new idea. Before this recent wave of attempts, the crypto industry and traditional financial institutions had long explored, but most of them ended in failure.

TheFTX exchange, which was once in the limelight, also provided US stock tokenization trading services including Tesla, GameStop, etc. from 2020 to 2022. However, FTX's collapse in 2022 brought this business to an abrupt end. Afterwards, rumors questioned whether FTX's stock tokens held the corresponding shares in full, further undermining the market's trust in the exchange's issuance of tokenized shares.

In 2021, Binance also tried to launch tokenized stock products corresponding to US stocks such as Tesla, Coinbase, and Apple, and users can purchase fractionalized shares of these stock tokens. However, regulations in various countries are tightening, and within weeks of Binance launching stock tokens, financial regulators in the UK and Germany have warned that these products may violate securities regulations. Less than three months later, Binance announced the delisting of all stock tokens.

In addition, Bittrex Global, an exchange that once featured tokenized stock trading, also chose to close its trading platform and go into bankruptcy liquidation after experiencing regulatory pressure and SEC lawsuits.

It can be seen that in the last round of attempts, compliance obstacles were the main reason for the failure of the tokenization of US stocks issued by exchanges. Now that the market is re-mentioning the tokenization of US stocks, there are the following factors:

1. With the Trump administration's emphasis and support for crypto, the tension between cryptocurrencies and regulation has also eased.

2. The market has entered a period of weakness, and the market needs some narrative returns supported by real value.

3. The technology and compliance plan is more mature. Compared with the previous barbaric growth, today's crypto market pays more attention to compliance design and technical guarantees. For example, Backed, each token received an EU-approved prospectus before issuance, clarifying the token holder's interest in the underlying shares. In terms of technology, the performance of oracles and public chains has been improved by an order of magnitude.

1 in 1,000 and trillion dollars expected: the real dilemma of tokenized stocks

Despite the impressive growth rate, there is still a huge gap between the actual market size of tokenized stocks and institutional forecasts. In essence, whether it is the tokenization of US stocks or the tokenization of other securities products, it can be classified as an RWA asset type. It's just that cryptocurrencies are both highly volatile and highly liquid financial assets like U.S. stocks, and the trading scale and capital volume of U.S. stocks, as well as the high-quality fundamentals of U.S. stock assets, are what the crypto world desires.

Theindustry is extremely optimistic about the future of stock tokenization, with some authorities predicting that the tokenized asset market will reach trillions of dollars around 2030: for example, the Boston Consulting Group (BCG) estimates that global tokenized assets will reach $16 trillion by 2030. The Security Token Market report even predicts that $30 trillion in assets will be tokenized by 2030, with stocks, real estate, bonds, and gold being the main drivers.

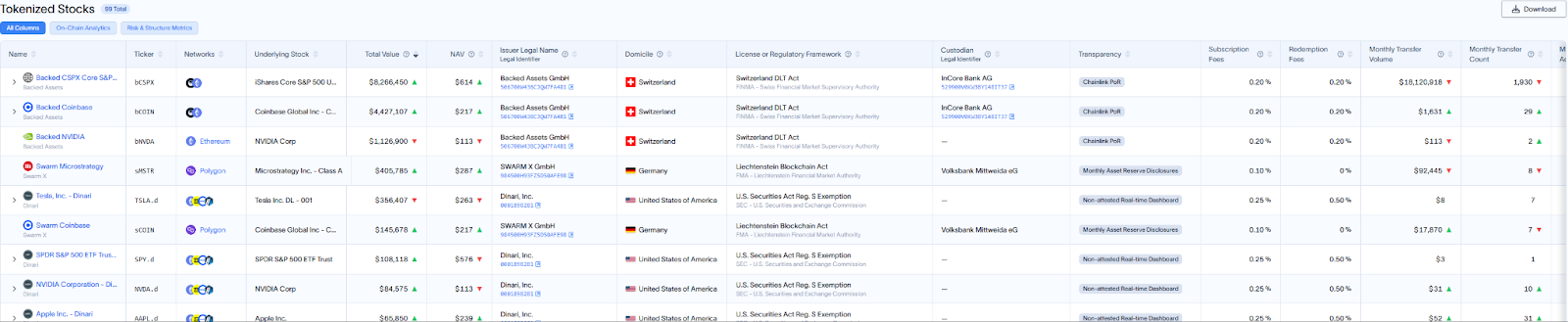

As of March 11, the total on-chain assets of global RWAs were about $17.8 billion, of which the total value of equity assets was about $15.43 million, accounting for less than 1/1,000, and the transaction volume for the whole month was only $18 million. Obviously, stock tokenization is still an immature market in the RWA track.

However, tokenized stocks are still competitive in terms of growth rate and risk resistance. In July 2024, the total on-chain value of tokenized shares was only about $50 million, an increase of about 3 times in half a year. This growth rate is significantly higher than the capital growth rate of other altcoin assets in the same period.

Recently, the crypto market has ushered in a sharp correction, with Bitcoin falling below 80,000, and the market capitalization of the entire crypto market has pulled back to the level of the first half of 2024, with a decline of 30% in the past three months. However, tokenized stocks performed significantly better during the same period, still at historical highs. It can be seen that the overall volatility of the U.S. stock market is much less affected by a single asset than the crypto market, and the fluctuation laws of different types of assets are not synchronized, resulting in the overall market looking more stable. This also provides a new value anchor for tokenized stocks.

For today's investors, U.S. stock tokenization is neither a bear market savior nor a short-lived concept. It is more like a seed that needs to wait patiently to break the ground - with the triangular support of compliance, technology and market sentiment, whether this seed can grow into a towering tree, the answer may be hidden in the SEC's next policy release, Coinbase's next compliance move, or the flow of funds from retail investors and institutions in the next bull market. The only thing that is certain is that this experiment is far from over.