When stablecoins begin to "earn interest": a new crypto wealth in the tens of billions market, who is really helping you earn passive income?

Original Title: Stablecoin Update May 2025

Original Source: Artemis

Original Compilation: Bitpush

In the crypto market, stablecoins are no longer just "stable" – they are quietly helping you make money. From U.S. Treasury yields to perpetual contract arbitrage, yield-bearing stablecoins are becoming the new income engine for crypto investors. At present, there are dozens of related projects with a market value of more than $20 million, with a total value of more than $10 billion. In this article, we will break down the revenue sources of mainstream interest-earning stablecoins, and take stock of the most representative projects in the market to see who is really "making money" for you.

is an interest-bearing stablecoin?

Unlike regular stablecoins, such as USDT or USDC, which only serve as a store of value, interest-bearing stablecoins allow users to earn passive income during their holdings. Their core value lies in bringing additional income to coin holders through the underlying strategy while keeping the stablecoin price anchored.

How are the benefits generated?

There are various sources of income for interest-bearing stablecoins, which can be summarized into the following categories:

· Real World Asset (RWA) Investments: The protocol invests funds in real-world low-risk assets such as U.S. Treasury bonds, money market funds, or corporate bonds, and returns the proceeds from those investments to the holders.

· DeFi Strategy: The protocol deposits stablecoins into decentralized finance (DeFi) liquidity pools, conducts liquidity farming, or employs "delta-neutral" strategies to extract yield from market inefficiencies.

· Lending: The deposit is lent to the borrower, and the interest paid by the borrower becomes the income of the holder.

· Debt Support: The protocol allows users to lock up crypto assets as collateral and lend stablecoins. The income is primarily derived from stability fees or interest generated on non-stablecoin collateral.

· Hybrid Sources: Yield comes from a variety of combinations such as tokenized RWA, DeFi protocols, and centralized finance (CeFi) platforms to achieve diversified returns.

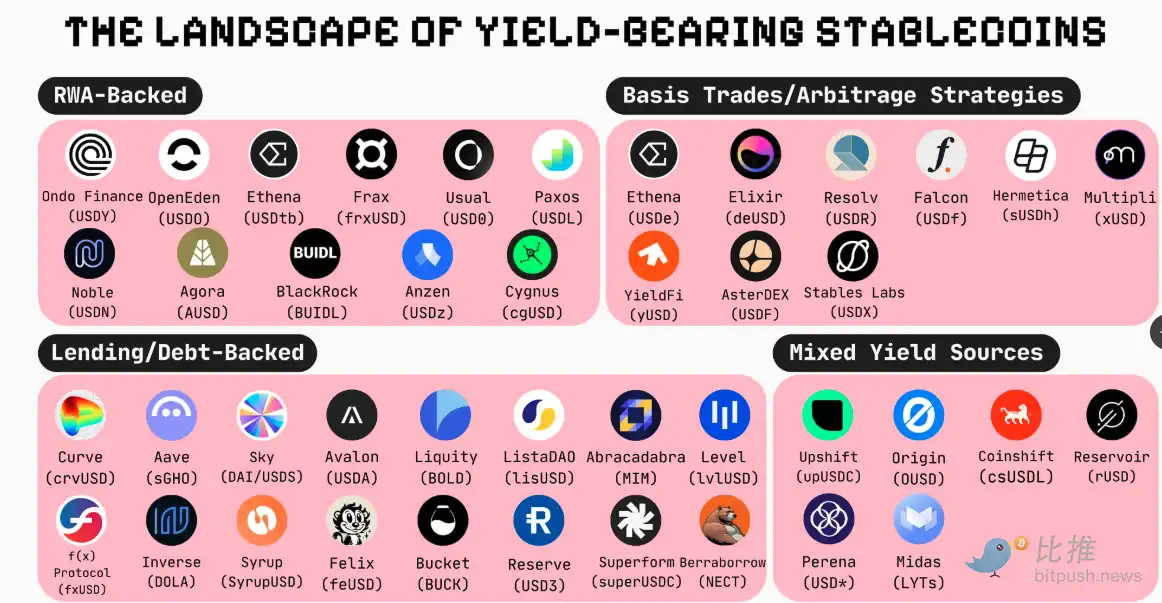

A quick overview of the interest-earning stablecoin market landscape (projects with a total supply of about $20 million and above)

Here is a list of some of the current mainstream interest-bearing stablecoin projects, categorized according to their main yield generation strategies. Please note that the data is for the total supply, and the list mainly covers interest-bearing stablecoins with a total supply of $20 million or more.

1. Stablecoins such as RWA-backed (primarily through U.S. Treasuries, corporate bonds, or commercial paper, etc.)

generate returns by investing money in real-world, low-risk, yielding assets.

· Ethena Labs (USDtb – $1.3 billion): Backed by BlackRock's BUIDL fund.

· Usual (USD0 – $619 million): Liquidity deposit token of the Usual protocol, backed 1:1 by ultra-short-term RWA (specifically aggregated US Treasury tokens).

· BUIDL ($570 million): BlackRock's tokenized fund that holds U.S. Treasuries and cash equivalents.

· Ondo Finance (USDY – $560 million): Fully backed by U.S. Treasuries.

· OpenEden (USDO – $280 million): Proceeds come from U.S. Treasuries and repo-backed reserves.

· Anzen (USDz – $122.8 million): Fully backed by a diversified portfolio of tokenized RWAs, consisting primarily of private credit assets.

· Noble (USDN – $106.9 million): Composable interest-bearing stablecoin, backed by 103% of US Treasuries, leveraging M0 infrastructure.

· Lift Dollar (USDL – $94 million): Issued by Paxos, fully backed by U.S. Treasuries and cash equivalents, and automatically compounded daily.

· Agora (AUSD – $89 million): Backed by Agora reserves, including USD and cash equivalents such as overnight reverse repos and short-term US Treasuries.

· Cygnus (cgUSD – $70.9 million): Backed by short-term Treasury bonds, it runs on the Base chain as a rebase-style ERC-20 token, with its balance automatically adjusted daily to reflect yields.

· Frax (frxUSD – $62.9 million): Upgraded from Frax Finance's stablecoin FRAX, it is a multi-chain stablecoin backed by BlackRock's BUIDL and Superstate.

2. Basis Trading/Arbitrage StrategyThis type of

stablecoin obtains income through market-neutral strategies, such as perpetual contract funding rate arbitrage, cross-trading platform arbitrage, etc.

· Ethena Labs (USDe – $6 billion): Backed by a diversified pool of assets, it maintains its peg through spot collateral delta hedging.

· Stables Labs (USDX – $671 million): Generate yield through a delta-neutral arbitrage strategy between multiple cryptocurrencies.

· Falcon Stable (USDf – $573 million): Backed by a portfolio of cryptocurrencies, yielding yield through Falcon's market-neutral strategies (funding rate arbitrage, cross-platform trading, native staking, and liquidity provision).

· Resolv Labs (USR – $216 million): Fully backed by an ETH staking pool, ETH price risk is hedged through perpetual futures, and assets are managed by off-chain escrow.

· Elixir (deUSD – $172 million): Using stETH and sDAI as collateral, creates a delta-neutral position by shorting ETH and captures a positive funding rate.

· Aster (USDF – $110 million): Backed by crypto assets and corresponding short futures on AsterDEX.

· Nultipli.fi (xUSD/xUSDT – $65 million): Earn yield through market-neutral arbitrage (including Contango arbitrage and funding rate arbitrage) on centralized exchanges (CEXs).

· YieldFi (yUSD – $23 million): Backed by USDC and other stablecoins, yields come from Delta-neutral strategies, lending platforms, and yield trading protocols.

· Hermetica (USDh – $5.5 million): Backed by Delta hedged Bitcoin, using short-selling perpetual futures on major centralized exchanges to earn funding.

3. Lending/Debt-Backed Stablecoins

generate returns by lending deposits, charging interest, or by collateralizing the stability fees and liquidation proceeds of debt positions (CDPs).

· Sky (DAI – $5.3 billion): Based on CDP (Collateralized Debt Position). Minted by staking ETH (LSTs), BTC LSTs, and sUSDS on @sparkdotfi. USDS is an upgraded version of DAI and is used to earn yield through Sky Savings Rate and SKY Rewards.

· Curve Finance (crvUSD – $840 million): An overcollateralized stablecoin, backed by ETH and managed by LLAMMA, whose peg is maintained through Curve's liquidity pools and DeFi integrations.

· Syrup (syrupUSDC – $631 million): Backed by a fixed-rate mortgage provided to crypto institutions, the proceeds are managed by @maplefinance's credit underwriting and lending infrastructure.

· MIM_Spell (MIM – $241 million): An overcollateralized stablecoin minted by locking interest-bearing cryptocurrency into Cauldrons, with proceeds derived from interest and liquidation fees.

· Aave (GHO – $251 million): minted through collateral provided in the Aave v3 lending marketplace.

· Inverse (DOLA – $200 million): A debt-backed stablecoin minted through collateralized lending on FiRM, with yield generated by staking into sDOLA, which earns self-lending income.

· Level (lvlUSD – $184 million): Backed by USDC or USDT deposited into DeFi lending protocols (such as Aave) to generate yield.

· Beraborrow (NECT – $169 million): Berachain's native CDP stablecoin, backed by iBGT. Yields are generated through liquidity stabilization pools, liquidation yields, and leverage boosts for PoL incentives.

· Avalon Labs (USDa – $193 million): A full-chain stablecoin minted using assets such as BTC through the CeDeFi CDP model, offering fixed-rate lending and generating yield by staking in the Avalon vault.

· Liquity Protocol (BOLD – $95 million): Backed by over-collateralized ETH (LSTs) and generating sustainable yield through interest payments from borrowers and ETH liquidation proceeds earned through its Stability Pools.

· Lista Dao (lisUSD – $62.9 million): An overcollateralized stablecoin on BNB Chain, minted by using BNB, ETH (LSTs), stablecoins as collateral.

· f(x) Protocol (fxUSD – $65 million): minted through leveraged xPOSITIONs backed by stETH or WBTC, with yields derived from stETH staking, opening fees, and stability pool incentives.

· Bucket Protocol (BUCK – $72 million): An over-collateralized CDP based on @SuiNetwork backed stablecoin, minted by staking SUI.

· Felix (feUSD – $71 million): Liquity fork CDP on @HyperliquidX. feUSD is an overcollateralized CDP stablecoin that is minted using HYPE or UBTC as collateral.

· Superform Labs (superUSDC – $51 million): USDC-backed vault that is automatically rebalanced to top-tier lending protocols (Aave, Fluid, Morpho, Euler) on Ethereum and Base, powered by Yearn v3.

· Reserve (USD3 – $49 million): Backed 1:1 by a basket of blue-chip interest-bearing tokens (pyUSD, sDAI, and cUSDC).

4. Hybrid income sources (combining DeFi, traditional finance, centralized finance income) are stablecoins that combine multiple strategies to diversify risk and optimize returns.

· Reservoir (rUSD – $230.5 million): An overcollateralized stablecoin backed by RWAs and a combination of USD-based capital allocators and lending vaults.

· Coinshift (csUSDL – $126.6 million): Backed by T-Bills and DeFi lending via Morpho, it offers regulated, low-risk returns through a vault curated by @SteakhouseFi.

· Midas (mEGDE, mTBILL, mMEV, mBASIS, mRe7YIELD – $110 million): Compliant institutional-grade stablecoin strategy. LYTs represent claims on actively managed interest-bearing RWA and DeFi strategies.

· Upshift (upUSDC – $32.8 million): Earns interest and is partially supported by a lending strategy, but yields are also derived from LP (liquidity provision), staking.

· Perena (USD*- $19.9 million): Solana's native interest-bearing stablecoin, which is at the heart of the Perena AMM and earns yield through swap fees and an IBT-powered liquidity pool.

To summarize

the above, interest-earning stablecoins with a total supply of around $20 million or more are highlighted, but keep in mind that all interest-earning stablecoins come with risks. Yields are not risk-free, and they may be subject to smart contract risk, protocol risk, market risk, or collateral risk, among other things.

Link to original article